Analysis on the Role of Digital Currencies in Economies

Current crises such as the global Corona crisis (Sars-COV-19) can mean that citizens are increasingly looking for secure forms of investment to cope with crises as well as digital payment options to avoid contact with pathogens for payment transactions. One possibility for this can be digital currencies. — Authors: Laila Ohk, Duc Au, Alexander Zureck

1. Problem Statement and Research Objective

The origin of digital money lies in the digital, decentralized Bitcoin, which was initially issued in 2008. In addition to Bitcoin, there are over 5,600 other cryptocurrencies as of June 2021. However, the term digital currency is not synonymous with the term cryptocurrency. In addition to cryptocurrencies, stablecoins belong to the group of digital currencies. The digital currencies of the central banks are called Central Bank Digital Currencies or CBDCs. The objective of the given article is to address the current discussion about the possibility of digital currencies to substitute cash as well as fiat money.

2. Theoretical Foundation of Money

According to the German Bundesbank, the concept of money is defined by its recognition as a means of payment. The quality (e.g. book money, banknotes, digital money) is insignificant. In contrast to this is the concept of currency. A currency is characterized by the fact that it is the official money issued by state institutions (Deutsche Bundesbank, 2019, w/o p.). For a good or a currency to be recognized as a means of payment in an economy, it must fulfil specific functions of money (Borchert, 2013, p.27; Thiele et al., 2017, p.3). The first function of money is that it is recognized as a unit of account and thus forms the basis for economic transactions (Mankiw, 2017, p.98). In economic transactions, money is referred to as the so-called “numéraire”, that is, a general unit of reference or yardstick. The function of the computing unit enables prices to be expressed or debts to be recorded (Borchert, 2013, p.29; Mankiw, 2017, p.99). Furthermore, money has the function of a store of value. Money earned today can be spent later or used to accumulate assets (Borchert, 2013, p.29). Due to inflation and deflation, the store of value function is an imperfect function. There is no guarantee that the value of money will last in the future (Mankiw, 2017, p.98). Should the domestic legal currency be exposed to stronger inflationary tendencies than, for example, foreign currencies, the foreign currency could be used in part. This can lead to a “functional split”, as the store of value function is taken over by another currency, metal, or the like. At the same time, the domestic currency will continue to be used as a medium of exchange (Borchert, 2013, p.29).

3. Introduction to Digital Currencies

Digital currencies and their underlying technologies are seen as the “next step in the evolution of money” (Maurer et al., 2013, p.273). When it comes to digital currencies, the terms electronic money (in short: e-money) and virtual money are often used arbitrarily interchangeable. Although they are closely related, the terms must be separated from one another. On the other hand, there is the physical money known today: fiat currencies. The term Fiat currency comes from the Latin and stands for ““it will””. In this context, fiat money is described as “money by order”. The fiat money used today is characterized by the fact that it is not tied to any material good but receives its value “by arrangement” from the central banks (Herger, 2016, p.67).

According to the German law on the supervision of payment services (Zahlungsdiensteaufsichtsgesetz; in short: ZAG) § 1 (2), electronic money is referred to as electronically stored monetary value that is issued to the issuer in return for payment of a sum of money and which is generally (of natural and legal persons) recognized. The stored value changes in its amount depending on the purchases and sales of the owner (European Central Bank, 2001, p.82). This means that e-money electronically represents a physical currency and, like fiat money, can be used as desired. In addition, e-money has a value-storing function and excessive fluctuations in value are not to be assumed (Welzel, 2013, p.217). E-money can be divided into two categories: software-based and hardware-based e-money. Software-based e-money means the storage of e-money in an online payment account. In contrast, there is hardware-based e-money, which is tied to a physical card (Europäische Kommission, 2018, p.2). Digital central bank currencies such as the e-krona or a potential e-euro are also e-money. However, it has not (yet) been defined whether these will be set up on a software or hardware basis (Häring, 2017, p.14).

The introduction of e-money has advantages for both issuers and users. Issuers assume an increase in efficiency and quality, a reduction in costs, an expansion of the product range and increased customer loyalty (Hartmann, 2000, p.68). In addition, the issuing e-money institutions have the option of accessing their users’ account information with their consent (limited to 90 days). In this way, the issuers can view data on lifestyle and purchasing habits, available financial framework, party affiliation, religion, etc. and use this data to gain a competitive advantage (Kühn, 2019, p.53). For the user, the greatest advantage is the simplified handling (Hartmann, 2000, p.68).

Virtual currencies are not to be understood as a further development of the traditional fiat money system with euros and US dollars. Virtual currencies are a completely new form of money that is not based on gold or previously existing currencies (Kasprowicz & Rieger, 2000, p.252). Thus, cryptocurrencies should not be seen as the next step in the evolution of money, but as a revolution (Maurer et al., 2013, p. 273). The concept of virtual currencies is to be equated with the concept of cryptocurrencies. There are currently around 9,000 cryptocurrencies (Groß et al., 2020, p.712). According to market capitalization, the best-known cryptocurrency is by far Bitcoin, as of March 2022 (CoinMarketCap, 2022, w/o p.).

Figure 1: Market capitalization of the largest cryptocurrencies (in US-Dollar); Source: Coinmarketcap (04.03.2022)

4. Empirical Findings

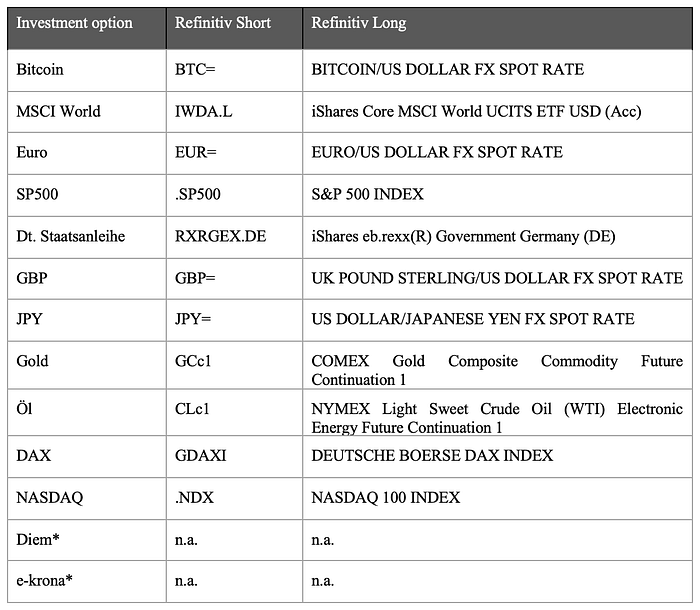

After the advantages and disadvantages of the individual digital currencies have been determined, three quantitative analyzes are carried out below. The aim of the first analysis is to check to what extent Bitcoin, Diem and e-krona are suitable as alternative investment vehicles for portfolio diversification. The second analysis aims to compare the volatility of different types of investment. The third analysis should show whether the course of the share price shows a positive or negative trend overall. The data used for the analysis are shown in Table 3. The daily closing price was selected for the analysis. In addition, the analysis was limited to the days of the week Monday to Friday, as only the Bitcoin is traded on the weekend. The last five years were chosen as the period (07/22/2016 to 07/22/2021). There is no data yet for the digital currencies Diem and e-krona, as they are still in a test phase. Correspondingly, the correlation with Bitcoin, Morgan Stanley Capital International (short: MSCI) World, Euro, Standard & Poor’s (short: SP) 500, German government bonds, Great Britain Pound (short: GBP), Japanese Yen (short: JPY), Gold, oil, German stock index (short: DAX) and National Association of Securities Dealers Automated Quotations (short: NASDAQ) is tested.

Table 3: Data sources; Sources: data taken from Refinitiv

The first analysis should check to what extent Bitcoin, Diem and e-krona are suitable as alternative investment vehicles for portfolio diversification. The formula used is the Pearson Correlation Coefficient. The correlation analysis shows that the Bitcoin is strongly correlated with the price of the MSCI World, SP500, and NASDAQ. A lighter correlation can be seen with the Euro, GBP, gold and the DAX. Bitcoin has a negative correlation with German government bonds. No or very little correlation can be seen with JPY and oil. Since the Bitcoin correlates with various forms of investment in the analysis, it must be checked whether this is due to the Corona crisis. A slump was recorded in some price developments in March and April 2020. The interruptions during the course are due to public holidays on which no trading took place. The analyzed graphic showed that some of the price developments saw a slump in March and April 2020, presumably due to the Corona crisis. The DAX, NASDAQ, Bitcoin and SP500 are affected. Other values such as gold did not develop noticeably during this time. The correlation analysis is therefore carried out again without the out-of-sample (OOS for short) data. OOS data is filtered to smooth out outliers in long-term samples. They are also often used for predictions. For this correlation analysis, it makes sense to carry out this without the OOS data, since the prices generally collapsed in March and April and thus the results of the correlation may have been falsified. The period in the following analysis is therefore again the past five years (07/22/2016 to 07/22/2021) excluding the months of March and April 2020. If correlations have occurred due to the Corona crisis, they are smoothed in this calculation. The correlation analysis carried out gives similar analysis results as before: A strong correlation with the MSCI World, SP500 and NASDAQ; medium strong correlation with Euro, GBP, gold, and DAX; negative correlation with German government bonds and finally a very low correlation with JPY and oil. The results show that a portfolio diversification through the Bitcoin offers itself in relation to German government bonds, since the price of these is opposite to that of the Bitcoin. Furthermore, a portfolio consisting of JPY and oil can be expanded by Bitcoin, as there is no correlation to these types of investments.

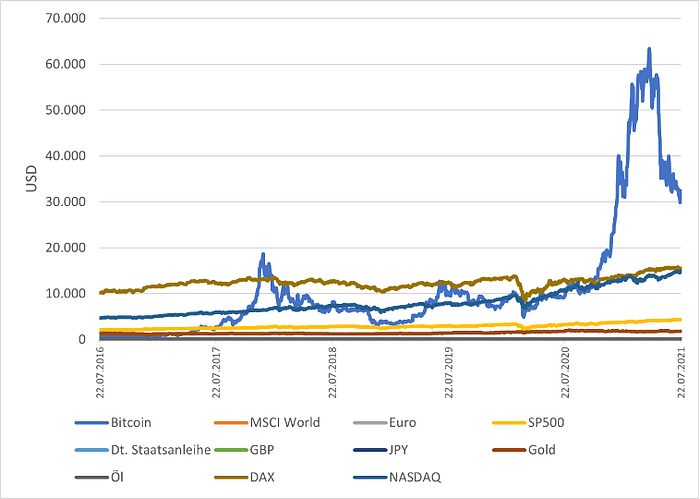

In the second analysis, the various investment options are to be examined for their volatility. Previously, it was already described in this article that Bitcoin shows high volatility. This should be checked with the following analysis. The same data is used as in the first analysis. First, a comparison of the volatilities is shown graphically.

Figure 4: Volatility of various types of investments — graphic analysis; Sources: data taken from Refinitiv

The graph shows that Bitcoin is much more volatile than the other investment options. To verify this, the volatility is checked below using the standard deviation. The analysis was carried out once including and once excluding the OOS months March and April 2020. The analysis of the standard deviation shows that Bitcoin has by far the largest standard deviation and thus the highest volatility. This can also be seen in the analysis excluding the months of March and April 2020. The recommendations for action derived from this result are explained in the next chapter.

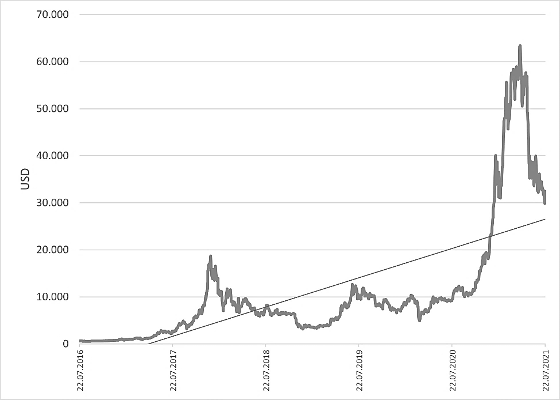

The third analysis will analyze the trend of the Bitcoin course. To analyze the trend, a trend line, and the simple moving average (SMA for short) are shown graphically on the one hand. The data already described, including March and April 2020, are used as the data basis. Figure 5 shows the trend line of the Bitcoin price.

Figure 5: Volatility of various types of investments — graphic analysis; Sources: data taken from Refinitiv

In the previous figure a trend line with a positive slope can be seen. This shows that, despite its volatility, Bitcoin has increased in value overall. The SMA enables price developments to be analyzed with smoothed fluctuations. The SMA with a 50-day interval also shows significant volatility in the Bitcoin price. Nevertheless, a positive development can also be observed here over the past five years. The analysis of the Trendline and the SMA has shown that Bitcoin has risen tendentially over the course of the year.

5. Critical Appreciation and Recommendations

Before recommendations for action are given, the results are critically assessed. It should be noted that the analysis results are findings that are linked to current circumstances. Due to their technological nature, digital currencies are exposed to dynamic processes so that the results may change in the future (Hanl & Michaelis, 2017, p.363). Also, regarding the not yet realized currencies e-krona and Diem, it must be pointed out that important technical and organizational details have not yet been finally defined (Groß et ao., 2019, p.631). Thus, the assumptions made regarding the influence on monetary policy, for example, have so far only been guesses. How the Diem and e-krona will affect monetary policy and other areas remains to be seen. It is also a research limitation that the quantitative analysis could only be carried out for the Bitcoin. Diem and e-krona have not yet been introduced and therefore no market data is available. It should also be noted that the Corona crisis, despite the OOS calculations without the months of March and April 2020, has an impact on the results and the results are to be viewed critically from this point of view. Despite the criticism, it can be assumed that Bitcoin, Diem and e-krona will play a relevant role in the future financial world.

Remarks

We are aware that Facebook is now Meta and that the project for the Diem has been cancelled. Nevertheless, the research was conducted before that announcement and we still believe the findings may contribute to the community.

About the authors

Laila Ohk is currently doing her Master of Science at Westfälische Wilhelms-Universität Münster. Laila has been working four years at RWE and is an experienced professional in Corporate Transformation.

Cam-Duc Au is currently doing his PhD at the Masaryk University in Brno in the field of crypto robo-advisory. He works as Lecturer at FOM University of Applied Sciences for Economics and Management as well as Manager Holdings at P. Keppler Verlag.

Alexander Zureck is Professor of Banking & Finance at the FOM Hochschule für Oekonomie & Management in Düsseldorf. In addition, he works as a consultant in business administration for medium-sized companies. He has been a member of the bdvb since 2010 and on the board of the regional association Ruhr-West.

Bibliography

Ali, R., Barrdear, J., Clews, R., & Southgate, J. (2014). Innovations in Payment Technologies and the Emergence of Digital Currencies. Bank of England Quarterly Bulletin 2014 Q3.

Borchert, M. (2013). Geld und Kredit: Einführung in die Geldtheorie und Geldpolitik (8. Auflage). München: Oldenbourg Wissenschaftsverlag.

CoinMarketCap. (2022). Today’s Cryptocurrency Prices by Market Cap. Abgerufen von https://coinmarketcap.com/1/ [Zugriff 2022–03–04]

Deutsche Bundesbank. (2019). Was ist Geld? Abgerufen von https://www.

bundesbank.de/de/service/schule-und-bildung/erklaerfilme/was-ist-geld — 800972 [Zugriff 2021–07–30]

Dörner, A., Mallien, J., Müller, M., Neuhaus, A., & Rezmer, A. (2021). Erst Bitcoin-Einbruch, dann Dogecoin-Boom: Wie Elon Musk die Krypto-Kurse bewegt. Handelsblatt.

Europäische Kommission. (2018). Bericht der Kommission an das europäische Parlament und den Rat über die Umsetzung und die Auswirkungen der Richtlinie 2009/110/EG und insbesondere über die Anwendung der aufsichtsrechtlichen Anforderungen an E-Geld Institute.

Europäische Zentralbank. (2001). Elektronisches Geld als Zahlungsmittel.

E-Commerce und E-Payment, 83–101.

eurostat. (o. J.). Glossary:In-sample vs. out-of-sample forecasts. Abgerufen von https://ec.europa.eu/eurostat/statistics-explained/index.php?title=

Glossary:In-sample_vs._out-of-sample_forecasts [Zugriff 2021–07–30]

GP. Bullhound. (2018). Token Frenzy.

Grigo, J., & Hansen, P. (2019). Digitalwährungen stehen vor dem Durchbruch. ifo Schnelldienst, 72(17), 6–8.

Groß, J., Herz, B., & Schiller, J. (2019). Libra — Concept and Policy Implications. Wirtschaftsdienst, 99(9), 625–631.

Groß, J., Herz, B., & Schiller, J. (2020). Bitcoin, Libra und digitale Zentralbankwährungen — ein Geldsystem der Zukunft? Wirtschaftsdienst, 100(9), 712–717.

Groß, J., Klein, M., & Sandner, P. (2020). Central Bank Digital Currencies: Benefits, Risks and the Role of Blockchain Technology. Wirtschaftsdienst, 100(7), 545–549.

Groß, J., & Seeser, S. (2020). Wie funktioniert Bitcoin?

Hanl, A., & Michaelis, J. (2017). Kryptowährungen — ein Problem für die Geldpolitik? Wirtschaftsdienst, 97(5), 363.

Häring, N. (2017). E-Geld statt Cash. Handelsblatt, Nr. 209, 14.

Hartmann, M. E. (2000). E-Geld als Zahlungsmittelinnovation: Mosaiksplitter oder Meilenstein? Elektronisches Geld und Geldpolitik, 67–134.

Herger, N. (2016). Wie funktionieren Zentralbanken? : Geld- und Währungs-politik verstehen. Wiesbaden: Springer Gabler.

investing.com. (2021). All Cryptocurrencies. Abgerufen von https://www.

investing.com/crypto/currencies [Zugriff 2021–07–30]

Kasprowicz, D., & Rieger, S. (2020). Handbuch Virtualität. Wiesbaden: Springer VS.

Kellermann, P. (2013). Kurze Geschichte des Geldes (Gold und Geld). In Soziologie des Geldes : Grundlegende und zeithistorische Einsichten (S. 3–6). Wiesbaden: Springer Fachmedien Wiesbaden.

Kühn, I. (2019). Der direkte Weg. Der Handel, (7–8), 52–53.

Lagarde, C. (2020). Payments in a digital world.

Lauren, S., & Harlili, S. D. (2014). Stock trend prediction using simple moving average supported by news classification. 2014 International Conference of Advanced Informatics: Concept, Theory and Application (ICAICTA), 135–139.

Libra Association Members. (2020). White Paper v2.0.

Lindeberg, R., & Ummelas, O. (2021). Swedish Central Bank Reveals First Study of Digital Currency. Bloomberg.

Livni, E. (2021). Cryptocurrency prices stabilize after another wild weekend. The New York Times.

Mankiw, N. G. (2017). Makroökonomik. Stuttgart: Schäffer Poeschel.

Maurer, B., Nelms, T., & Swartz, L. (2013). “When perhaps the real problem is money itself!”: the practical materiality of Bitcoin. Social Semiotics, 23(2), 261–277.

Müller, M. (2021). Elon Musk verhilft Kryptowährung Dogecoin zu Kurs-gewinnen. Handelsblatt.

Peren, F. W. (2020). Formelsammlung Wirtschaftsstatistik: Wissen kompakt für Studierende und Praktiker.

Praekhaow, P. (2010). Determination of trading points using the moving average methods. International Conference for a Substation Greater Mekong Sub-Region, GMSTEC.

Sveriges Riksbank. (2017). The Riksbank’s e-krona project. (Report 1).

Szalay, E., & Stafford, P. (2021). Bitcoin flash crash amplified by leverage and ‘systemic issues’. Financial Times.

Thiele, C.-L., Diehl, M., Mayer, T., Elsner, D., Pecksen, G., Brühl, V., & Michaelis, J. (2017). Kryptowährung Bitcoin: Währungswettbewerb oder Spekulationsobjekt: Welche Konsequenzen sind für das aktuelle Geldsystem zu erwarten? ifo Schnelldienst, (22), 3–20.

Welzel, P. (2013). Elektronisches Geld: Herausforderung für die Wirtschafts-politik? Transatlantik: Transfer von Politik, Wirtschaft und Kultur, 215.